For capital-intensive industries in Louisiana, managing property taxes is a game of long-term strategy. Programs like the Industrial Tax Exemption Program (ITEP) provide incredible relief, but they also create a ticking clock.

What happens when that 10-year exemption clock finally runs out?

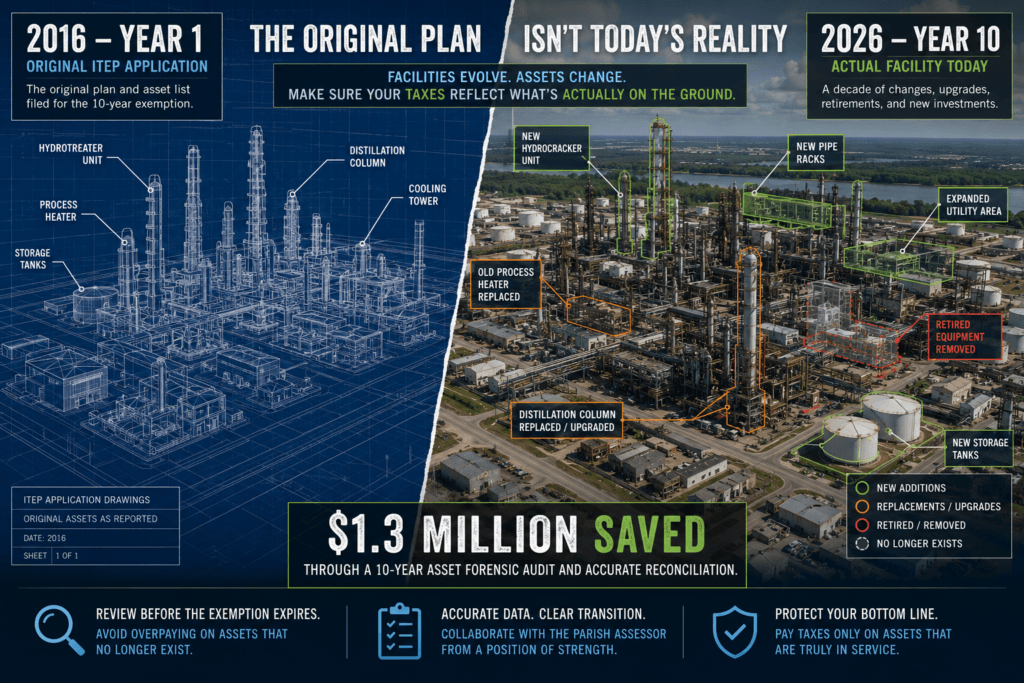

Too many companies assume the transition from “exempt” to “taxable” will be seamless. In reality, it can trigger a massive, inflated tax bill if you aren’t proactive. We recently helped a client navigate this exact scenario, turning a potential financial shock into a $1.3 million tax savings victory.

Here is how we did it—and why waiting until the exemption expires is the biggest mistake you can make.

When a 10-year property tax exemption rolls off, the Parish Assessor’s job is to put those assets onto the active tax roll. But assessors aren’t mind readers, and they don’t track your day-to-day operations.

In this case, the Parish Assessor took the easiest logical path: they grabbed the original cost from the exemption application filed a decade ago and dropped it directly onto the current tax roll.

There was just one massive issue. A manufacturing or industrial site looks vastly different in Year 10 than it did in Year 1. Over a decade, things change. Assets get retired, replaced, or cannibalized for parts. By simply copying and pasting old data, the parish was taxing our client on “ghost assets”—items that hadn’t been on the physical site for years.

To fix the overvaluation, our team had to reconstruct a decade’s worth of industrial history. We didn’t just look at the original application; we did a deep dive into the client’s comprehensive asset details.

Our review tracked:

By reconciling a decade of messy, real-world data against the original application, we built an undeniable, audit-ready case showing that the actual taxable value on the ground was significantly lower than what was on paper.

Armed with hard data, we sat down with the Parish Assessor to negotiate a settlement. Because our methodology was transparent and backed by concrete asset tracking, we were able to reach a landmark agreement:

If there is one takeaway from this success story, it is this: The time to review assets under exemption is before they hit the tax roll.

If you wait until the assessor issues the bill, you are playing defense. The assessor gets caught off guard by sudden, drastic drops in expected parish revenue, which naturally invites skepticism, friction, and protracted legal battles.

By conducting an asset review before the exemption rolls off, you can present a clean, accurate transition plan to the assessor. It fosters collaboration, prevents administrative whiplash, and—most importantly—ensures you never pay a single dollar of tax on an asset that no longer exists.

Is your Louisiana property tax exemption nearing its expiration date? Don’t let a decade-old piece of paper dictate tomorrow’s profits. Contact our team today for a proactive asset review.